Code

| country | lifeExp | pop | gdpPercap | |

|---|---|---|---|---|

| 10 | Afghanistan | 42.129 | 25268405 | 726.734055 |

| 22 | Albania | 75.651 | 3508512 | 4604.211737 |

| 34 | Algeria | 70.994 | 31287142 | 5288.040382 |

INF-604: Data Analysis

![]()

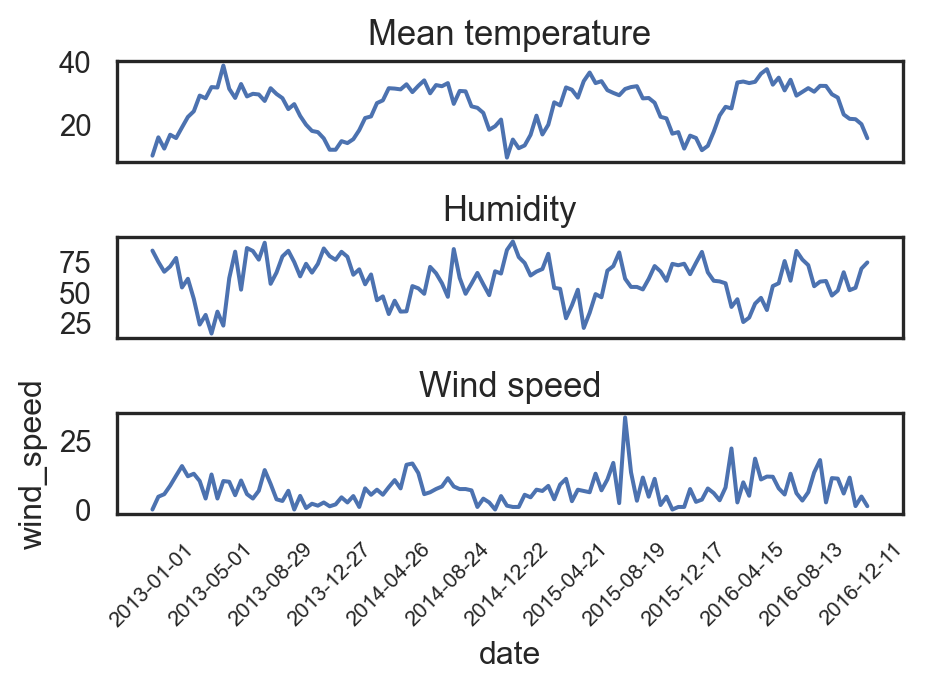

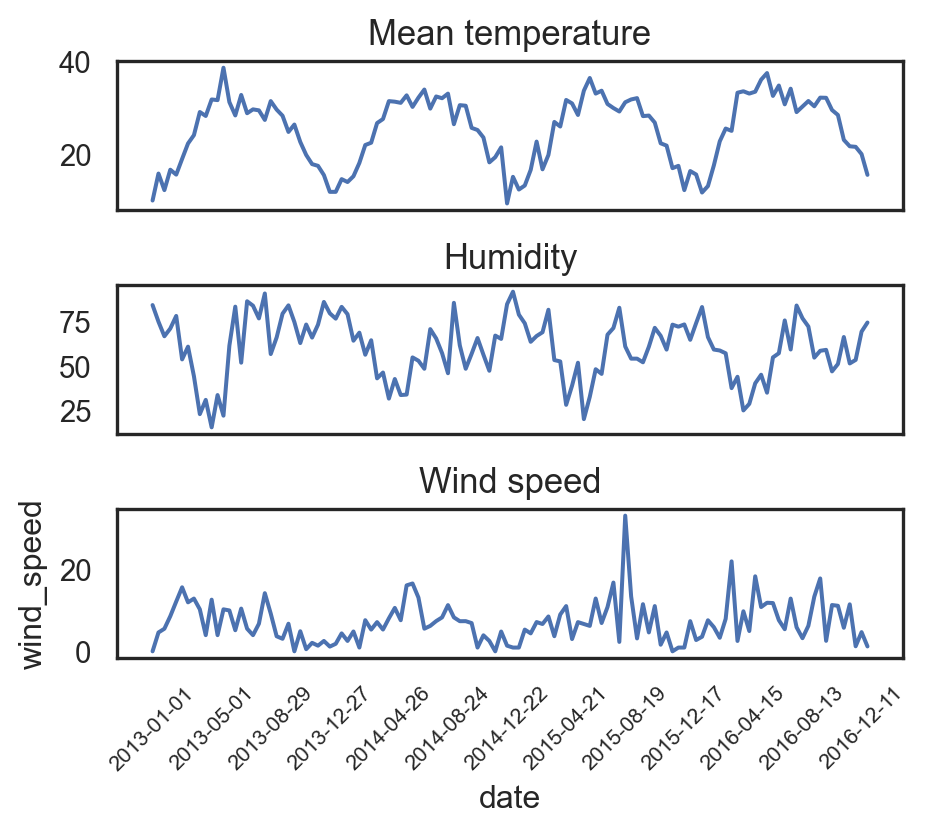

import matplotlib.pyplot as plt

sns.set(style="white")

_, axs = plt.subplots(3, 1, figsize=(5,4.5))

sns.lineplot(df_climate.iloc[::12,:], x="date", y="meantemp", ax=axs[0])

axs[0].set_title("Mean temperature", fontsize=13)

axs[0].set_xticks([])

axs[0].set_ylabel("")

axs[0].set_xlabel("")

sns.lineplot(df_climate.iloc[::12,:], x="date", y="humidity", ax=axs[1])

axs[1].set_title("Humidity", fontsize=13)

axs[1].set_xticks([])

axs[1].set_ylabel("")

axs[1].set_xlabel("")

sns.lineplot(df_climate.iloc[::12,:], x="date", y="wind_speed", ax=axs[2])

axs[2].set_title("Wind speed", fontsize=13)

# axs[2].tick_params(axis='x', labelrotation=90, size=8)

plt.xticks(df_climate.iloc[::12,:].date[::10], rotation=45, size=8)

plt.tight_layout()

plt.show()

import plotly.express as px

def cat_gdp(yearly_data):

return pd.qcut(yearly_data, q=3, labels=['Developing', 'Emerging', 'Developed'])

df = gapminder

# Apply the function to each year

df['GDP_Category'] = df.groupby('year').apply(lambda x: cat_gdp(x.gdpPercap)).reset_index(level=0, drop=True)

df_Af = df.query("continent == 'Asia'")

# Aggregate the data

df_agg = df_Af.groupby(['year', 'GDP_Category']).size().reset_index(name='Count')

# Create the stacked bar chart

fig = px.bar(

df_agg, x='year', y='Count',

color='GDP_Category', barmode='stack',

title="Evolution of Asian Countries' GDP from 1952 to 2007",

labels={'Count': 'Number of Countries', 'year': 'Year'})

fig.update_layout(height=410, width=500)

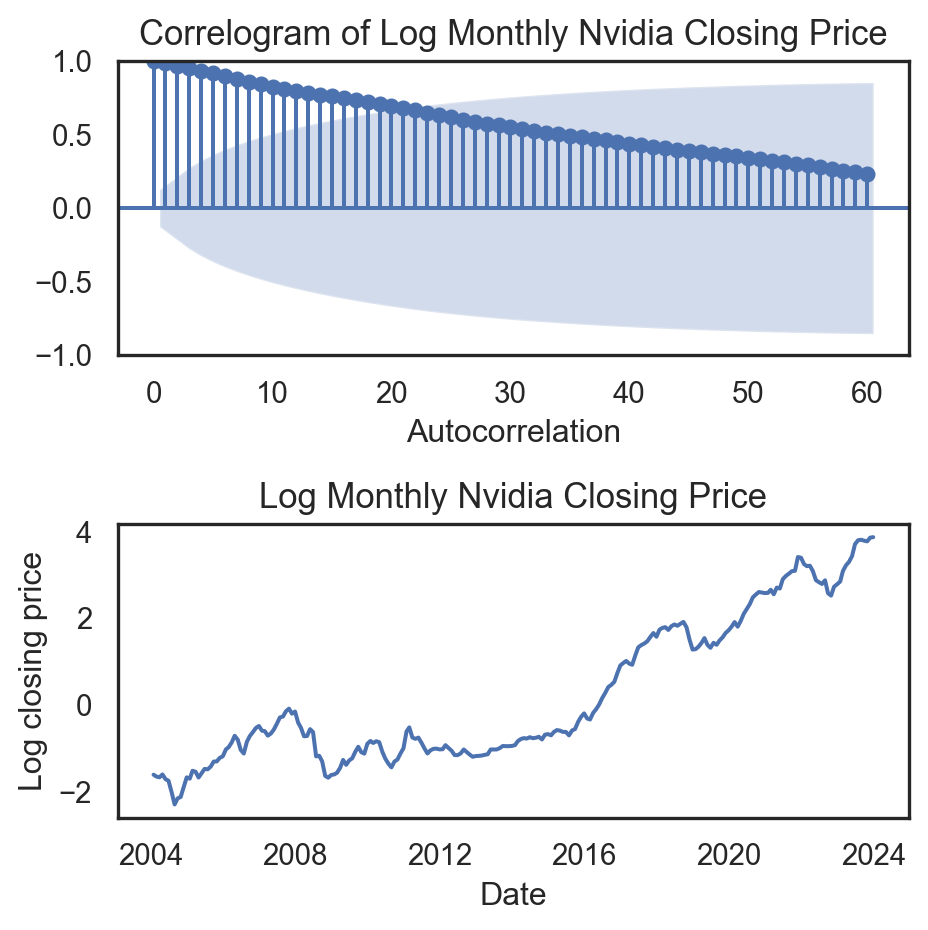

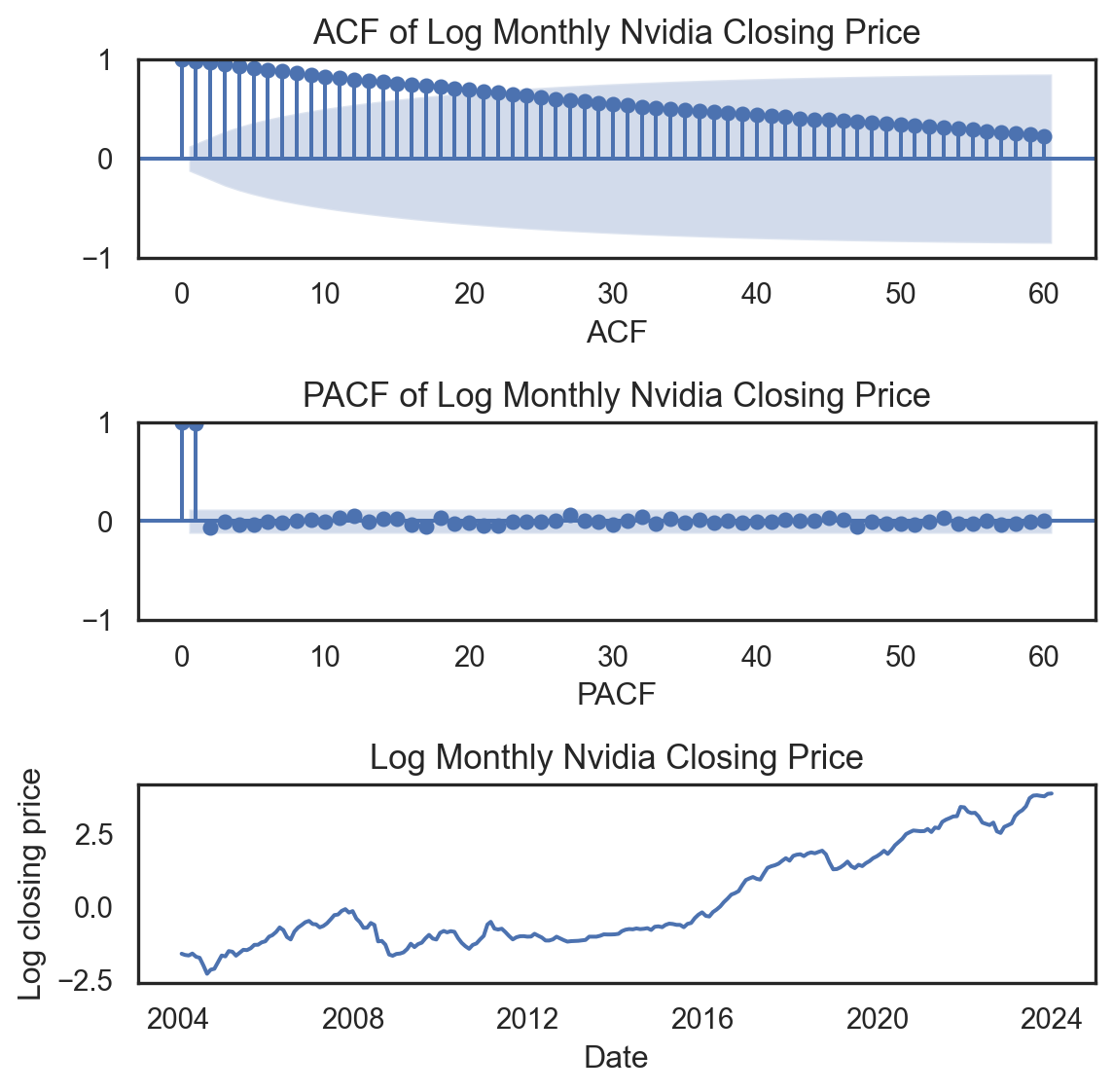

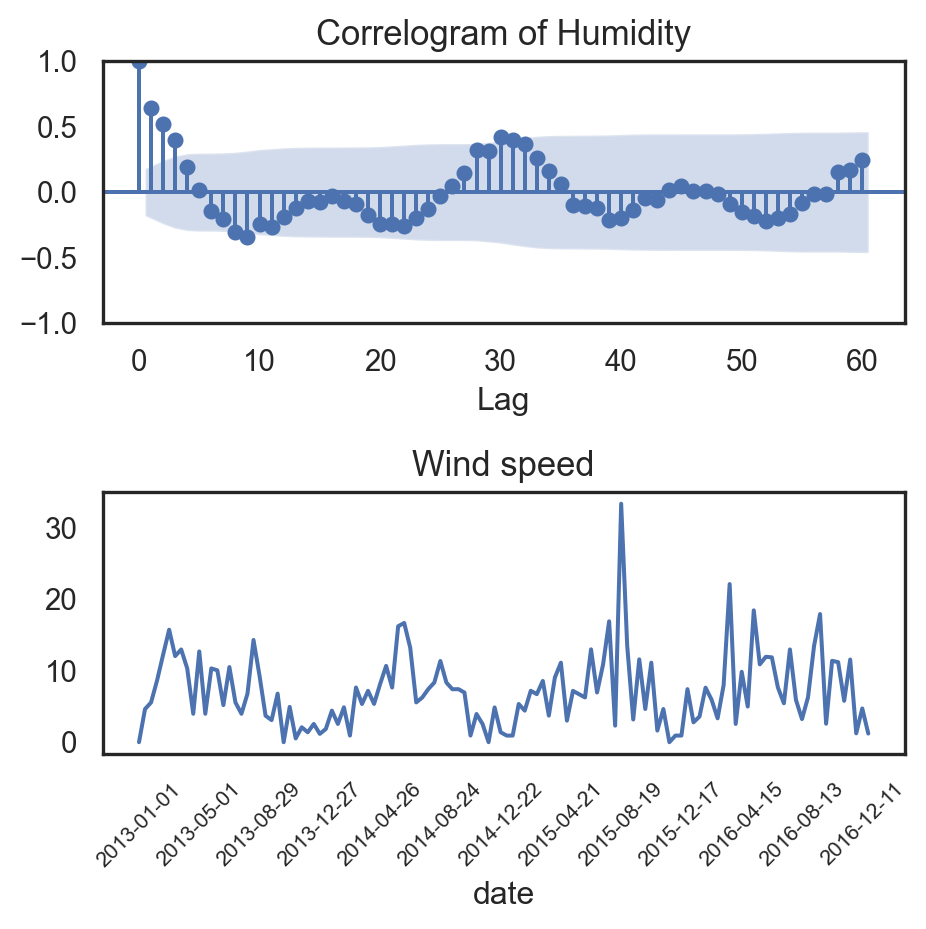

fig.show()from statsmodels.graphics.tsaplots import plot_acf

_, ax = plt.subplots(2,1,figsize=(6, 4))

plot_acf(df_lag.Temp, lags=60, ax=ax[0])

ax[0].set_title('Correlogram for Mean Temperature', fontsize=13)

ax[0].set_xlabel('Lag')

ax[0].set_ylabel('Autocorrelation')

sns.lineplot(df_climate.iloc[::12,:].iloc[:60,:], x="date", y="meantemp", ax=ax[1])

ax[1].set_title("Mean temperature", fontsize=13)

ax[1].set_ylabel("")

ax[1].set_xlabel("")

plt.xticks(df_climate.iloc[::12,:].iloc[:60,:].date[::10], rotation=45, size=8)

plt.tight_layout()

plt.show()

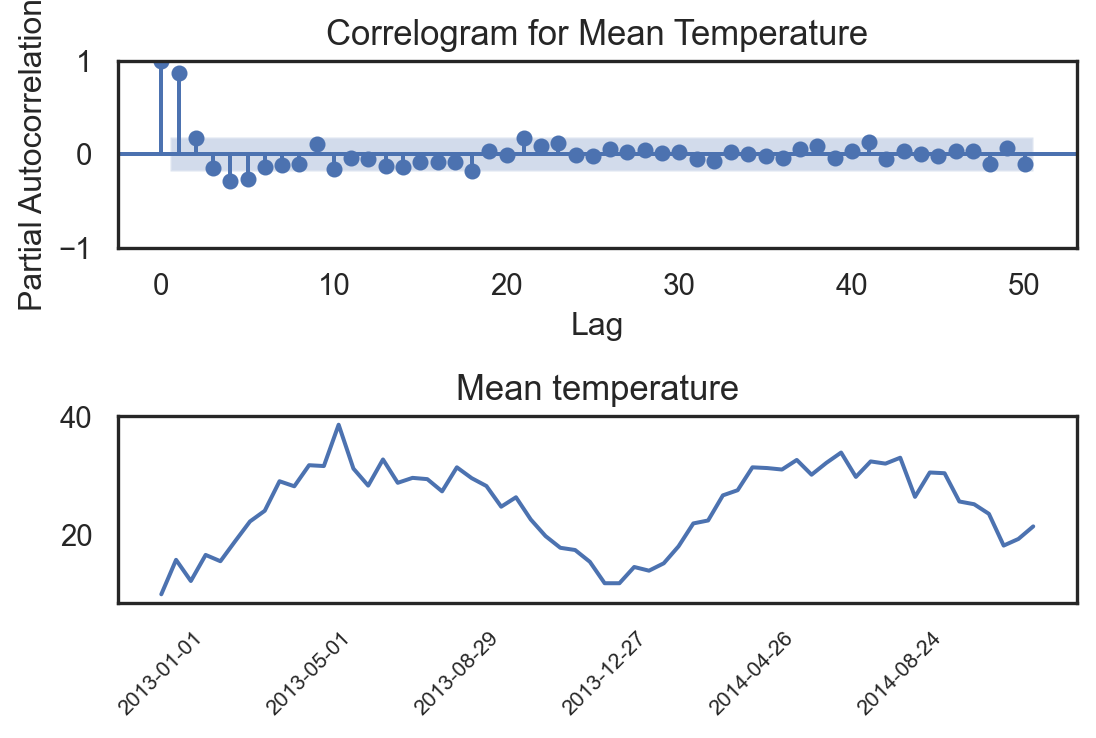

from statsmodels.graphics.tsaplots import plot_pacf

_, ax = plt.subplots(2,1,figsize=(6, 4))

plot_pacf(df_lag.Temp, lags=50, ax=ax[0])

ax[0].set_title('Correlogram for Mean Temperature', fontsize=13)

ax[0].set_xlabel('Lag')

ax[0].set_ylabel('Partial Autocorrelation')

sns.lineplot(df_climate.iloc[::12,:].iloc[:60,:], x="date", y="meantemp", ax=ax[1])

ax[1].set_title("Mean temperature", fontsize=13)

ax[1].set_ylabel("")

ax[1].set_xlabel("")

plt.xticks(df_climate.iloc[::12,:].iloc[:60,:].date[::10], rotation=45, size=8)

plt.tight_layout()

plt.show()

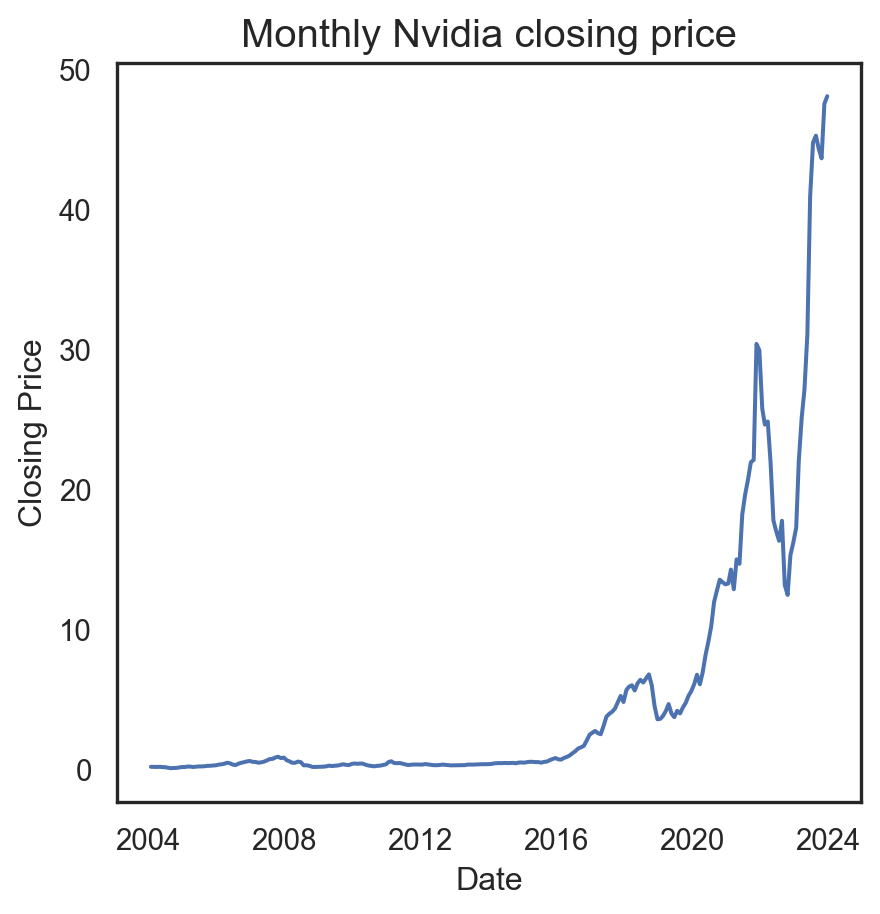

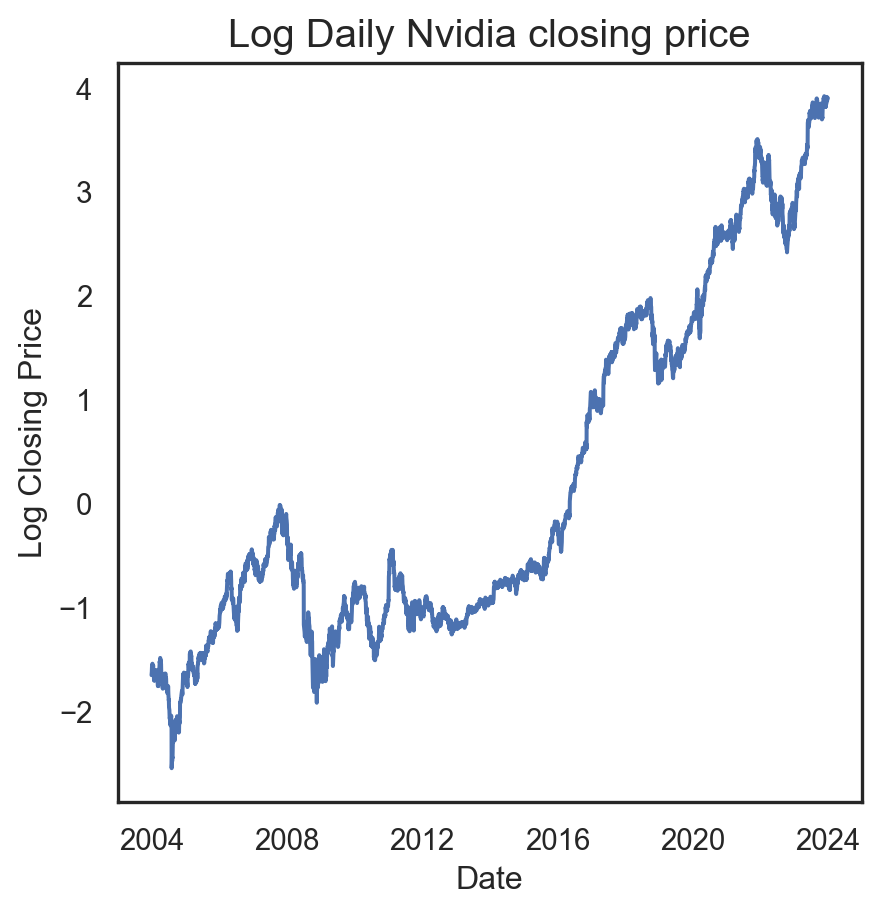

| Date | Open | High | Low | Close | |

|---|---|---|---|---|---|

| 0 | 2012-05-18 | 42.05 | 45.00 | 38.00 | 38.23 |

| 1 | 2012-05-21 | 36.53 | 36.66 | 33.00 | 34.03 |

| 2 | 2012-05-22 | 32.61 | 33.59 | 30.94 | 31.00 |

| 3 | 2012-05-23 | 31.37 | 32.50 | 31.36 | 32.00 |

| 4 | 2012-05-24 | 32.95 | 33.21 | 31.77 | 33.03 |

| 5 | 2012-05-25 | 32.90 | 32.95 | 31.11 | 31.91 |

| 6 | 2012-05-29 | 31.48 | 31.69 | 28.65 | 28.84 |

| 7 | 2012-05-30 | 28.70 | 29.55 | 27.86 | 28.19 |

| 8 | 2012-05-31 | 28.55 | 29.67 | 26.83 | 29.60 |

| 9 | 2012-06-01 | 28.89 | 29.15 | 27.39 | 27.72 |

| 10 | 2012-06-04 | 27.20 | 27.65 | 26.44 | 26.90 |

| 11 | 2012-06-05 | 26.70 | 27.76 | 25.75 | 25.87 |

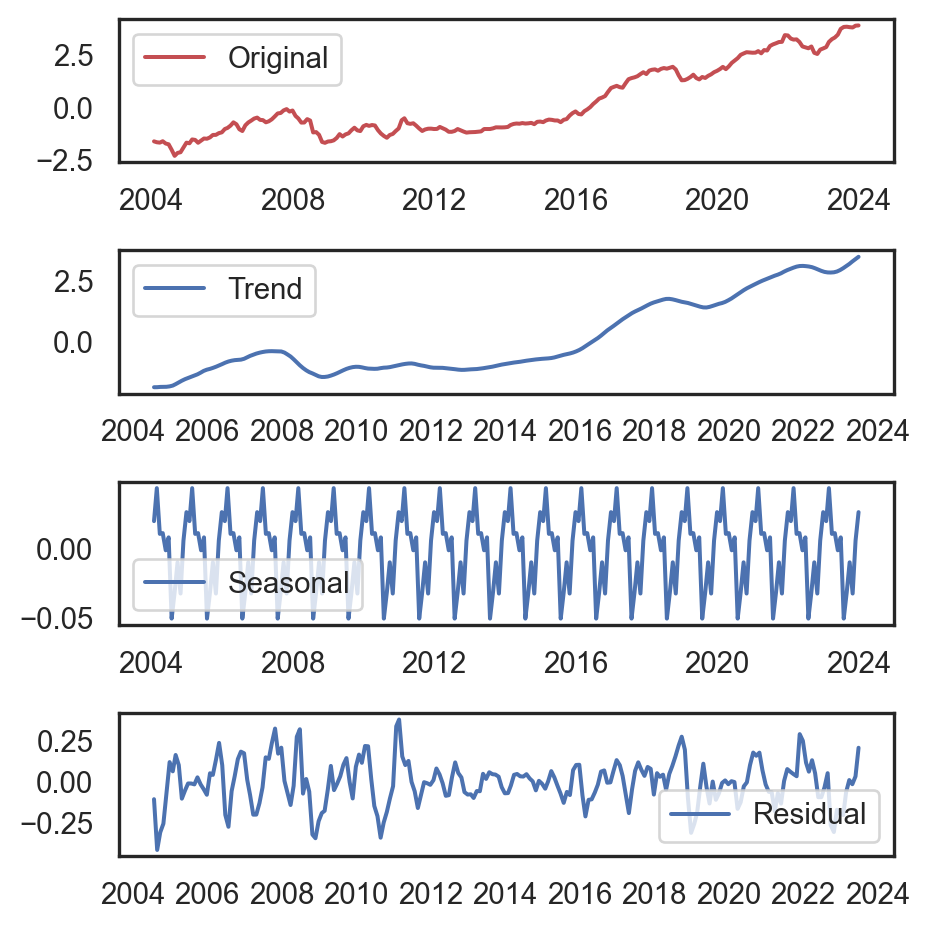

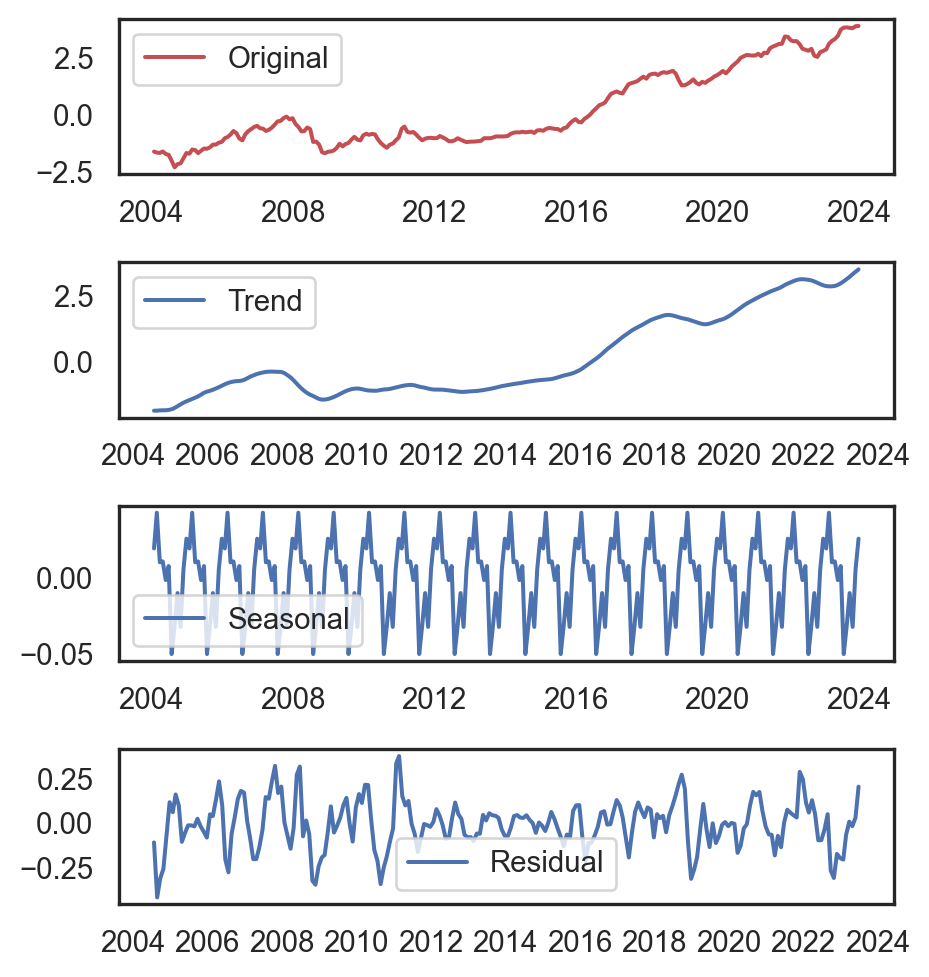

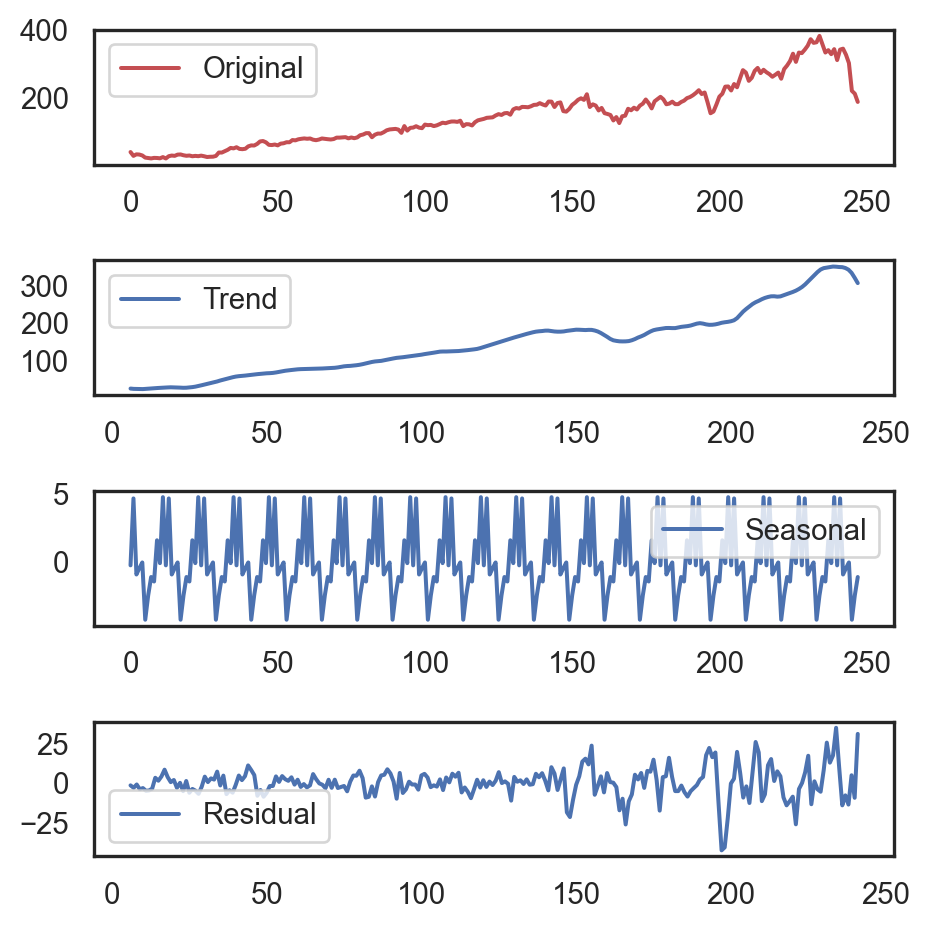

from statsmodels.tsa.seasonal import seasonal_decompose

ts = df_fb[['Close']].values[::10]

decomposition = seasonal_decompose(

ts, model='additive',

period=12)

seasonal, trend, residual = decomposition.seasonal, decomposition.trend, decomposition.resid

plt.figure(figsize=(5, 4.5))

plt.subplot(411)

plt.plot(ts, 'r', label='Original')

plt.legend()

plt.subplot(412)

plt.plot(trend, label='Trend')

plt.legend()

plt.subplot(413)

plt.plot(seasonal, label='Seasonal')

plt.legend()

plt.subplot(414)

plt.plot(residual, label='Residual')

plt.legend()

plt.tight_layout()

plt.show()

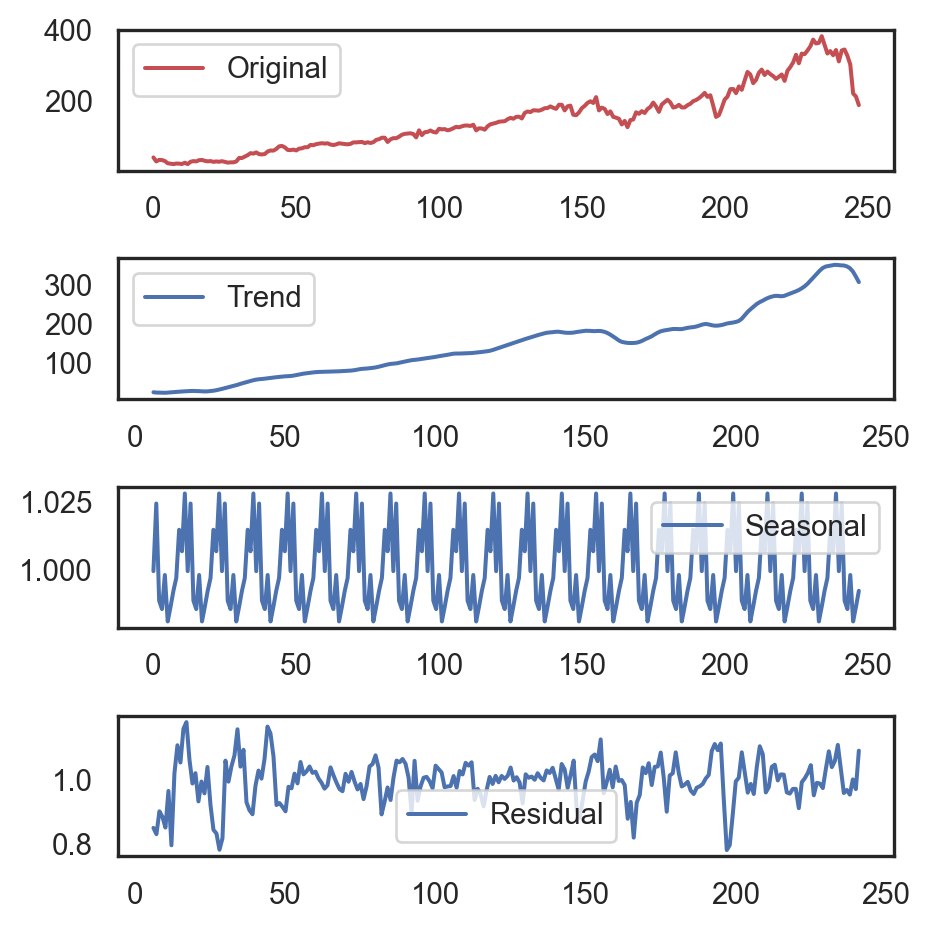

decomposition = seasonal_decompose(

ts, model='multiplicative',

period=12)

seasonal, trend, residual = decomposition.seasonal, decomposition.trend, decomposition.resid

plt.figure(figsize=(5, 4.5))

plt.subplot(411)

plt.plot(ts, 'r', label='Original')

plt.legend()

plt.subplot(412)

plt.plot(trend, label='Trend')

plt.legend()

plt.subplot(413)

plt.plot(seasonal, label='Seasonal')

plt.legend()

plt.subplot(414)

plt.plot(residual, label='Residual')

plt.legend()

plt.tight_layout()

plt.show()